CT1 Filing in Ireland

Every Irish company must file a Corporation Tax return, Form CT1, with Revenue every year. Miss the deadline and surcharges apply automatically. Get the iXBRL tagging wrong and the return is rejected. And in 2026, with the first Pillar Two filings also due, the stakes have never been higher.

Here is everything you need to know.

What Is Form CT1?

Form CT1 is the Corporation Tax return that every Irish company must file annually with the Revenue Commissioners, regardless of whether the company traded or made a profit during the year. It details taxable profits, deductions, tax liability, and any reliefs or credits claimed.

All CT1 returns must be filed electronically through the Revenue Online Service (ROS). Paper filing is not accepted.

CT1 Filing Deadlines 2026

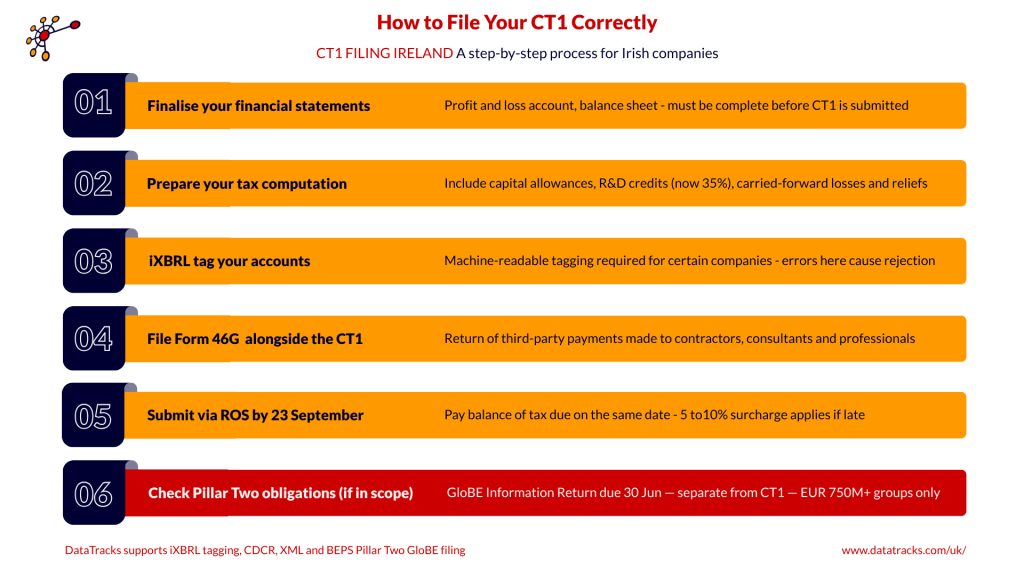

The CT1 must be filed nine months after the end of the accounting period, by the 23rd day of that ninth month when filing via ROS.

Accounting Year-End | CT1 Filing Deadline |

31 December 2025 | 23 September 2026 |

31 March 2025 | 23 December 2025 |

30 June 2025 | 23 March 2026 |

30 September 2025 | 23 June 2026 |

Large companies with a prior-year liability above €200,000 must pay preliminary tax based on 90% of the current year liability or 100% of the prior year, whichever is higher. Companies with a prior-year liability below €200,000 can base preliminary tax on 100% of the prior year.

Penalties for Late CT1 Filing

Getting the filing wrong is expensive. Revenue imposes the following surcharges on late CT1 returns:

How Late | Surcharge | Maximum Cap |

Within 2 months of deadline | 5% of tax liability | €12,695 |

More than 2 months late | 10% of tax liability | €63,485 |

In addition, daily interest of 0.0219% applies on any unpaid tax. Late filing can also result in loss of valuable reliefs including loss relief and group relief.

What Must Be Filed with the CT1?

Filing the CT1 form alone is not enough. Every CT1 submission must include:

- Finalised financial statements (profit and loss, balance sheet)

- Tax computation including capital allowances, R&D credits, and carried-forward losses

- Form 46G (return of third-party payments to contractors and consultants)

- iXBRL-tagged accounts where required

- Records of preliminary tax payments

How to File Your CT1 Correctly

iXBRL: Who Needs It and Why It Matters

iXBRL (Inline eXtensible Business Reporting Language) is mandatory for certain Irish companies filing with Revenue. iXBRL-tagged financial statements must be uploaded alongside the CT1 via ROS. The tagging makes financial data machine-readable, allowing Revenue to validate and process submissions more efficiently.

Errors in iXBRL tagging result in rejected filings and delays, even where the underlying tax figures are correct. This is one of the most common and most avoidable reasons for CT1 complications.

DataTracks is recognised as HMRC’s first managed tagging provider and processes iXBRL filings in Ireland with 99%+ accuracy, with turnaround times as fast as three days.

What’s New in 2026: Key Changes Affecting CT1 Filers

R&D Tax Credit Increased to 35%

The R&D tax credit increased from 30% to 35% for accounting periods starting on or after 1 January 2026, with the first-year payment threshold raised from €75,000 to €87,500. Companies claiming R&D relief must ensure their CT1 accurately captures this.

CATO Joint Filing Service Closed

The joint HMRC and Companies House filing service closed on 31 March 2026. Irish companies filing with both Revenue and the Companies Registration Office (CRO) must now manage these separately using commercial software.

Pillar Two: The Most Significant New Obligation in a Generation

This is the biggest change affecting large Irish companies in 2026 and it is entirely separate from the CT1. The first Pillar Two returns and top-up tax payments are due by 30 June 2026 for fiscal years ending 31 December 2024. This applies to multinational groups with consolidated global revenues of €750 million or more.

Ireland has implemented three Pillar Two mechanisms:

- QDTT (Qualified Domestic Top-Up Tax): Ensures Irish entities pay at least 15% effective tax rate in Ireland, keeping top-up tax revenue in Ireland rather than allowing other jurisdictions to collect it.

- IIR (Income Inclusion Rule): Requires the Ultimate Parent Entity to top up tax where constituent entities fall below 15%.

- UTPR (Undertaxed Profits Rule): Acts as a backstop where IIR does not apply.

Failure to file an IIR, UTPR or QDTT return by the return date gives rise to a penalty of €10,000. Where an entity fails to file an information return, the penalty is €10,000 per month up to a maximum of €480,000.

Safe harbour rules may exempt some groups from paying top-up tax, but registration and filing are still required. The GloBE Information Return (GIR) is a separate filing from the CT1 entirely. It requires 200+ data points per entity, jurisdiction-by-jurisdiction ETR calculations, and structured XML output.

How to Avoid CT1 Rejections and Penalties

- File via ROS well before the 23rd of the ninth month after your year-end

- Ensure iXBRL tagging is accurate before submission, not after rejection

- File Form 46G alongside the CT1

- Pay preliminary tax on time to avoid daily interest charges

- Register for Pillar Two obligations via ROS if your group is in scope

- Begin GloBE data collection early — the 30 June 2026 deadline for FY2024 is approaching fast

How DataTracks Helps Irish Companies File Compliantly

DataTracks supports Irish companies with accurate, compliant iXBRL tagging for Revenue CT1 submissions. With over 450,000 files filed globally and turnaround times as fast as three days, we ensure your financial statements are tagged correctly and accepted first time.

For groups with Pillar Two obligations, DataTracks also provides CbCR XML generation compliant with OECD Action 13 across 25+ countries, and BEPS Pillar Two GloBE Information Return support, giving you end-to-end coverage of Ireland’s most complex 2026 filing requirements.

Submit once. Get accepted.

Visit www.datatracks.com/uk/ to learn more about how we can help. For enquiries, email contact@datatracks.com or call +44 20 8834 9596.

Frequently Asked Questions

When is the CT1 filing deadline for a December 2025 year-end?

The CT1 must be filed by 23 September 2026 via ROS.

What happens if I file my CT1 late in Ireland?

A surcharge of 5% of the tax liability applies if filed within two months of the deadline, capped at €12,695. If filed more than two months late, the surcharge rises to 10%, capped at €63,485. Daily interest of 0.0219% also applies on unpaid tax.

Is iXBRL mandatory for Irish CT1 filings?

Yes, for certain companies. iXBRL-tagged financial statements must be uploaded via ROS with the CT1. Errors in tagging cause rejection even if the tax figures are correct.

What is the Pillar Two deadline for Irish companies in 2026?

The first Pillar Two information returns and top-up tax payments are due by 30 June 2026 for fiscal years ending 31 December 2024.

Is the Pillar Two GloBE return the same as the CT1?

No. The GloBE Information Return is a completely separate filing from the CT1, with its own deadlines, data requirements, and penalties.

Does Pillar Two affect Irish SMEs?

No. Pillar Two only applies to multinational groups with consolidated global revenues above €750 million. Irish SMEs continue under the standard 12.5% corporation tax rate.

How can DataTracks help with CT1 filing in Ireland?

DataTracks provides managed iXBRL tagging for Revenue CT1 submissions, CbCR XML generation, and BEPS Pillar Two GloBE reporting support, all with 99%+ accuracy and fast turnaround times.