Your client wishes to go public. The traditional IPO approach is on the table, deadlines are being established, and S-1 preparation is taking shape. Someone in the room then suggests, “Should we be looking at a SPAC instead?”

Two years ago, such a query seemed unlikely; today, it demands a real answer.

Special Purpose Acquisition Companies have maintained actual momentum through 2025 and into 2026, after experiencing a major decline following the 2021 boom and subsequent regulatory scrutiny. For capital market attorneys and general counsel guiding companies on their path to the public markets, SPACs are no longer a niche alternative or a shortcut for companies that do not qualify for a regular IPO. They’ve grown into a structurally distinct, governance-driven mechanism that belongs in any genuine IPO discussion.

This blog outlines what happened, why it is important, and what legal and compliance professionals should know to advise clients and file documents with confidence.

The Numbers That Tell the Story

The data for 2025 and early 2026 is startling. According to figures recorded as of early March 2026, 51 SPAC IPOs had priced year-to-date, accounting for 88% of the 58 total U.S. IPOs exceeding $40 million and raising $10.9 billion of the $13.9 billion in total proceeds. That’s not a specialized instrument. That is the primary IPO vehicle in the current market.

Zoom out to the full-year picture and the trend becomes even clearer:

The SPAC market refueled in 2025, with about 150 new mechanisms formed, which is more than 2023 and 2024 combined. In December 2025 alone, 28 new S-1 registration statements for SPAC IPOs were filed, with 22 deals completed and approximately $5.3 billion raised, a substantial increase from the rate in November.

These are not insignificant numbers for attorneys who advise on capital market transactions. They define the current landscape in which your clients operate.

How SPACs Evolved: From Shortcut to Strategic Instrument

Understanding where SPACs are now necessitates understanding where they originated from and why the 2021 version of a SPAC is not what attorneys and clients will be working with in 2026.

The 2021 Boom and Its Consequences

In 2021, 613 SPAC IPOs raised $162.5 billion, accounting for 63% of total IPO activity. The market was inundated with blank check companies, many of which were loosely structured, barely regulated, and more concerned with speed than quality. The regulatory scrutiny that followed led to a severe decrease following the 2021 boom. By 2023, the trough had arrived: only 31 SPAC IPOs, $3.8 billion raised, and 53 liquidations as projects failed to find suitable targets.

The Structural Rebuild: SPAC 3.0

The 2025 resurgence of SPACs marks a structural turning point rather than a short-lived rebound. This year’s momentum has been driven by stronger sponsors, improved governance, and a more selective investor base.

What does that mean in practice? The 2025–2026 vantage of SPACs looks materially different from 2021:

Tighter warrant structures: Reduced warrant coverage that limits dilution and is more acceptable to institutional investors.

Cleaner promoted economics: Cleaner promoted economics: Sponsored economics prioritize long-term success over guaranteed upside.

Stronger investor protections: Enhanced redemption rights and clearer deal disclosure standards.

Focused sector strategies: Today’s SPACs are targeting specific verticals, rather than broad categories, such as AI infrastructure, energy, industrial technology, and digital asset infrastructure.

The significant acquisitions from December 2025 clearly demonstrated this trend. Churchill Capital Corp XI, SilverBox Corp V, and Bitcoin Infrastructure Acquisition Corp. Ltd. all focused on industrial technologies, energy, and digital asset plumbing, rather than the speculative consumer conceptions that dominated the 2021 cycle.

The 2026 cohort of SPACs employs more specialized sector strategies than their predecessors, and under new SEC Chair Paul Atkins, the regulatory environment may become even more favorable for SPACs, with the agency refocusing on capital formation.

Why Every IPO Advisor Needs to Understand SPACs Right Now

The practical reality for capital market attorneys and general counsel is that your clients are considering both options at the same time, and your ability to advise on the SPAC pathway, including filing mechanics, disclosure obligations, and structural nuances, is now a core competency rather than an optional specialty.

- The De-SPAC Pathway Offers What Traditional IPOs Can’t Always Provide

A SPAC combination has specific advantages, particularly in an environment characterized by valuation sensitivity and selective investor demand. In 2025, de-SPACs will be more focused on creating a bespoke, negotiated, and partnership-driven entry into the public markets rather than avoiding the rigors of the IPO process.

The opportunity to negotiate valuation directly with a sponsor rather than going through a book-building process is a significant strategic advantage for growth-stage companies in capital-intensive industries. Understanding the S-4 merger proxy mechanics and the subsequent SEC reporting duties is critical for attorneys negotiating those transactions.

- The Filing Complexity Is Significant and Growing

A SPAC transaction entails numerous distinct SEC filings during its lifecycle:

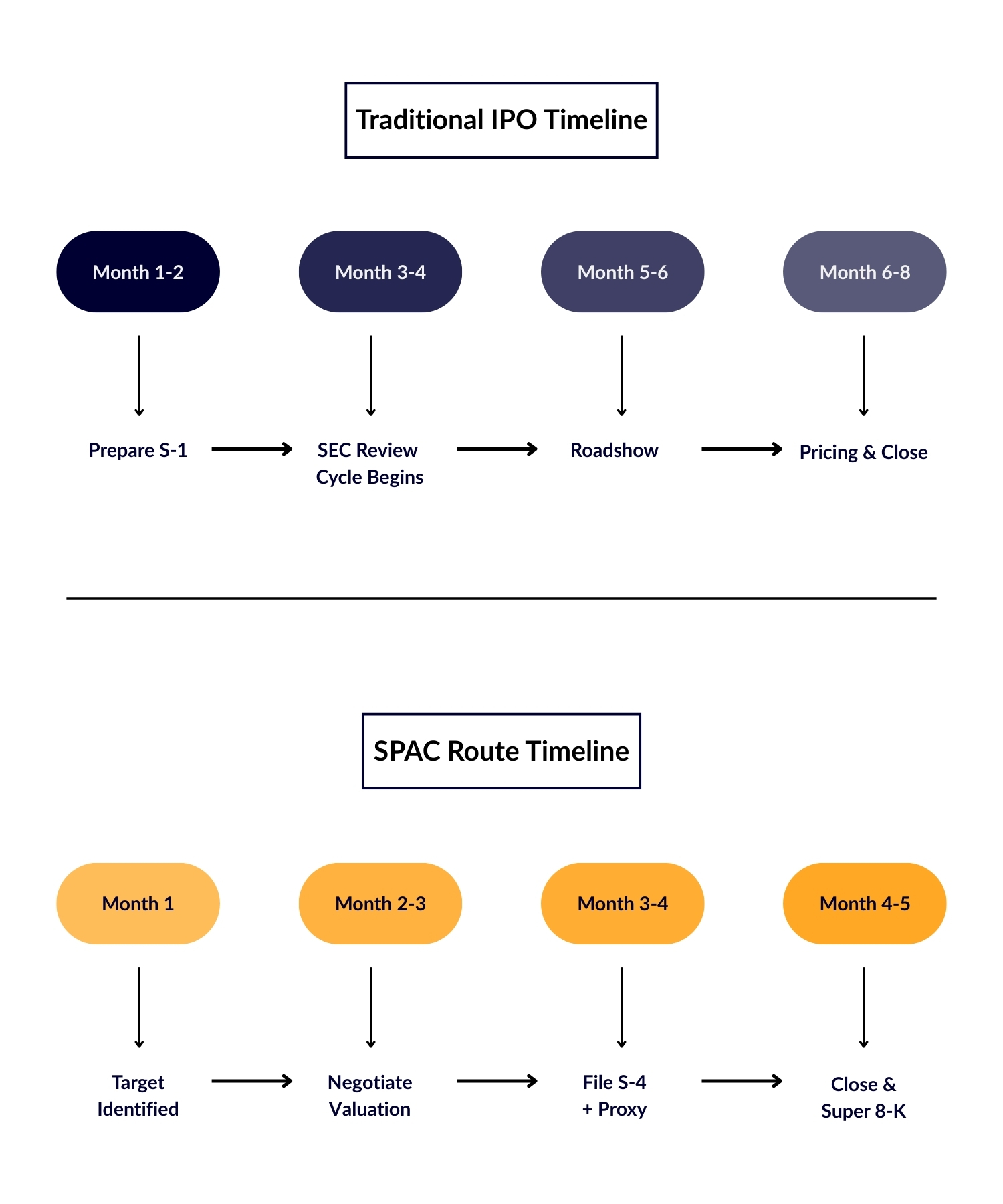

- S-1: The SPAC’s initial public offering registration.

- S-4 or Form F-4: The business combination registration statement.

- Super 8-K: Filed within four business days of deal closure, essentially serving as the de-SPAC company’s IPO filing.

- Ongoing 10-K, 10-Q, and 8-K obligations: Once the de-SPAC company is public, full reporting obligations apply immediately.

Each of these filings has XBRL and iXBRL tagging requirements. The SEC reviews the structured data incorporated in these documents, and institutional investors who consume EDGAR data programmatically are scrutinizing it more closely. Errors in tagging at any level of the SPAC lifecycle, from the S-1 to the post-merger 10-K, can result in SEC comment letters, transaction delays, and reputational issues at a vital point.

- The Pipeline Is Building Faster Than Teams Can Scale

As of early March 2026, 204 SPACs are actively seeking targets, 99 have announced deals, and the pipeline of prospective de-SPAC transactions is substantial as sponsors approach deployment deadlines. The growing number of SPACs with unredeemed trusts and ample time to transact opens new prospects for companies looking to list publicly.

For legal teams advising target companies, this means an increase in the number of SPAC approach conversations, each of which has the potential to become a transaction with a short filing timeframe.

The Filing Dimension: Where Deals Get Done or Derailed

Capital market attorneys understand that a SPAC transaction can be physically elegant and commercially solid, but it will still suffer significant friction if the SEC filing procedure is not handled with precision.

The Super 8-K is one of the most complex and important filings in the SPAC lifecycle. It must include audited financial statements, comprehensive XBRL-tagged disclosures, and a detailed business description for the combined firm within four business days of the transaction’s closing. That’s a timeline that allows no room for tagging errors, taxonomy mismatches, or EDGAR validation failures.

Similarly, the S-4 registration statement for the business combination requires substantial financial disclosure, pro forma financial statements, and iXBRL tagging that must perfectly adhere to the SEC’s structured data standards.

Legal teams that understand this complexity and have dependable SEC filing partners in place before the transaction clock begins are better positioned to advise clients, manage deadlines, and prevent last-minute filing scrambles that can jeopardize deals.

Actionable Steps for Capital Markets Legal Teams

To advise clients effectively on SPAC transactions in today’s market, legal and compliance teams should:

- Know both pathways: Understand the full SPAC filing lifecycle alongside the traditional IPO S-1 process, so you can give clients a genuinely comparative view.

- Engage SEC filing experts early: SPAC timelines compress quickly; having a filing partner in place before the transaction is announced avoids critical bottlenecks.

- Treat iXBRL compliance as a transaction risk factor: Structured data errors in S-4s and Super 8-Ks can cause SEC comment cycles, delaying deal closures.

- Monitor the pipeline actively: With 204 SPACs actively seeking targets, your customers in growing areas may receive SPAC approaches before a typical IPO process begins.

- Build post-merger reporting into the deal structure: The de-SPAC company’s first 10-K is often filed under significant time pressure; planning for that obligation during the transaction protects clients from post-close surprises.

How DataTracks Empowers Capital Markets Legal Teams

At DataTracks, we work at the intersection of regulatory compliance and transaction execution, exactly where SPAC filings live.

End-to-End SEC Filing Services DataTracks supports the whole SPAC filing lifecycle, including S-1 registrations, S-4 business combination statements, Super 8-Ks, and ongoing 10-K and 10-Q responsibilities after de-SPAC completion. Every stage of the transaction benefits from our team’s extensive EDGAR knowledge and structured data precision.

DataTracks Rainbow™ for iXBRL and XBRL Compliance Our cloud-based iXBRL platform automates XBRL tagging, enforces taxonomy rules, and performs real-time validations, removing the manual errors that cause comment letters and filing delays at the worst conceivable times in a deal’s timetable.

Explore our SEC Product DataTracks Rainbow™

Flexible, Transparent Pricing SPAC transactions do not have a set schedule, and neither should your filing support. DataTracks uses a clear, à la carte pricing model, which means legal teams may get expert filing support for certain documents, phases, or the entire transaction lifecycle at a price that scales with the deal.

Trusted by 30,000+ Companies Across 25+ Countries DataTracks has delivered over 300,000 reports across global regulatory regimes. When your client’s transaction timeframe is short and the filing date is set, depth of experience is critical.

Conclusion

SPACs have earned their position in the capital markets toolkit, not as a shortcut, but as a mature, governance-driven avenue that currently accounts for the majority of US IPO activity. The question for capital market attorneys and general counsel is no longer whether they should comprehend SPACs. It is whether your firm is prepared to advise on them, execute the necessary filings, and protect clients throughout the transaction’s lifecycle.

The structure has evolved. The filing challenges are genuine and the pipeline is expanding.

The firms that advise precisely and file correctly will define best-in-class SPAC counsel in 2026.

If you would like to know more about how DataTracks can support your SPAC and IPO filings from S-1 through post-merger reporting, then Explore our SEC Reporting Services or request a custom quote for your next transaction.