So, What Changed on January 17, 2026

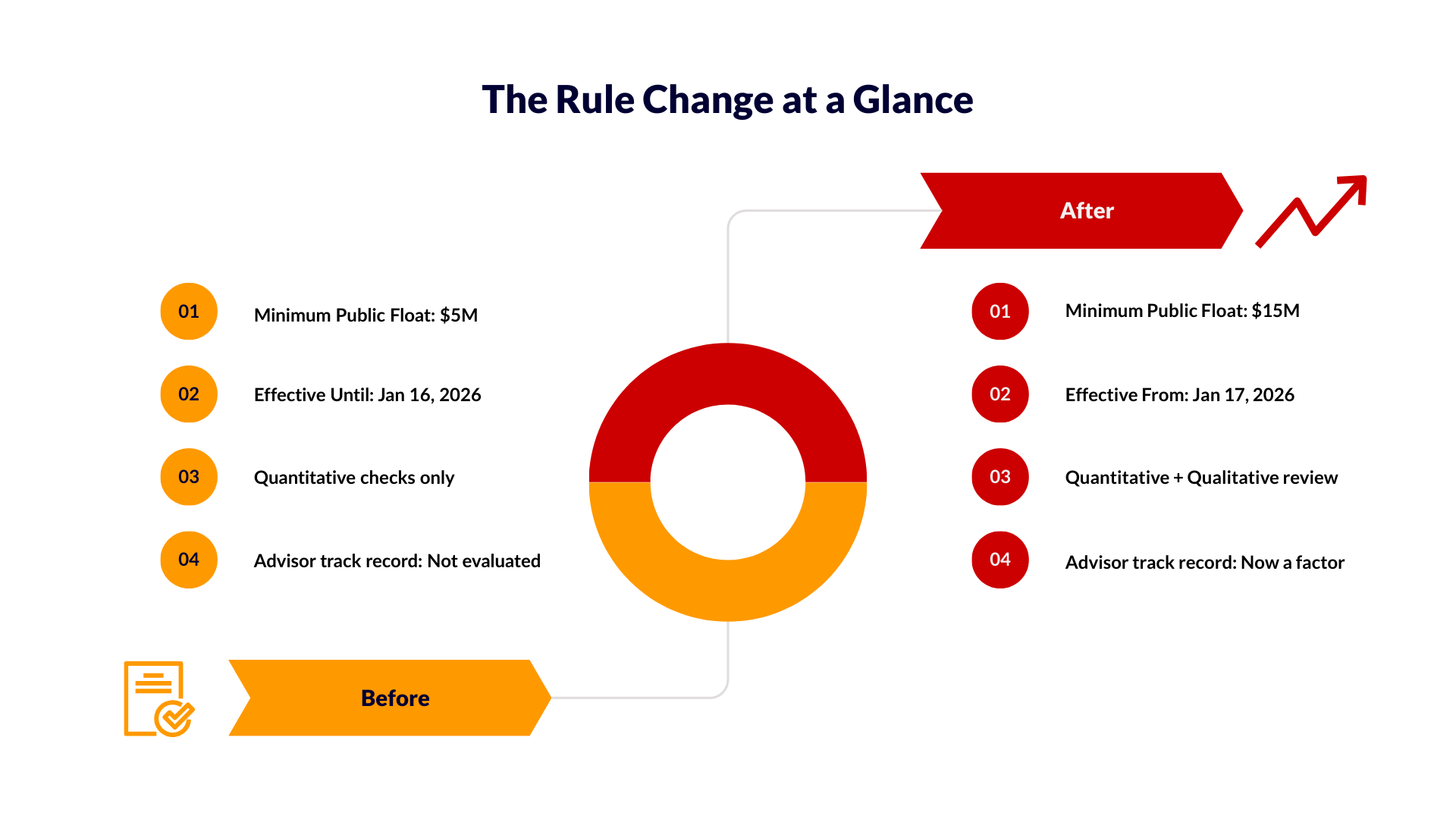

Your company has been preparing for a Nasdaq listing. Your financials are in order, your advisors are engaged, and your team has been working toward the moment you ring that opening bell. Then, on January 17, 2026, Nasdaq altered the rules, doubling the minimum public float requirement from $5 million to $15 million overnight. For many micro-cap companies, that’s not a minor adjustment. It represents a major shift in the requirements for listing.

But here’s what most coverage of this change has overlooked. The new float threshold isn’t even the most disruptive part of what just occurred.

Nasdaq now has the authority to reject your listing even if you meet every single quantitative requirement. And that changes everything about how micro-cap companies, and the financial professionals advising them, need to prepare.

For full listing standards, visit here

The Hidden Shift: Discretionary Authority Under Rule IM-5101-3

The float threshold dominates the headlines. But Rule IM-5101-3 is where the real disruption occurs.

Under this rule, Nasdaq now has considerable discretionary authority to decline a listing application even if the business meets all quantitative requirements.

What factors can result in discretionary denial? Nasdaq has stated that it may evaluate:

And still receive a rejection letter.

What Can Trigger Discretionary Denial?

Nasdaq has indicated it may evaluate:

-

Your advisors’ track record. Auditors, underwriters, and legal counsel previously associated with problematic listings may raise concerns.

-

Trading patterns of similar companies. If comparable companies experienced volatile or suspicious trading activity, your application may receive heightened scrutiny.

-

Market manipulation risk. Concerns related to shareholder composition, float structure, or trading characteristics.

-

Quality and credibility of your service providers. Your advisory team’s reputation has effectively become an unofficial listing criterion.

You can review regulatory context through the SEC’s rule approval documentation and Nasdaq’s interpretive material under Rule IM-5101-3.

This represents a significant departure from how the listing process traditionally operated. Previously, getting listed was largely a compliance exercise. Meet the numbers, file the documents, get approved.

Now, the process includes a qualitative review, where your advisors’ reputation is evaluated alongside your balance sheet.

How This Is Reshaping the Micro-Cap Listing Landscape

The micro-cap segment has long served as a critical entry point for growth companies seeking access to public funding. These new requirements create additional hurdles throughout the listing process.

1. A Higher Capital Bar Before You Even Begin

Micro-cap companies typically operate in capital-constrained environments.

The increase from $5 million to $15 million implies:

-

Greater pre-IPO fundraising

-

Increased dilution risk

-

Extended listing timelines

Companies that built strategies around the previous threshold must now recalibrate.

2. Advisor Selection Is Now a Listing Risk Factor

Under Rule IM-5101-3, your choice of auditor, underwriter, and legal counsel is no longer solely about expertise and cost. It is a listing risk variable.

Nasdaq may assess whether your service providers’ histories raise red flags. This places a premium on hiring advisors with clean, well-regarded track records in the micro-cap IPO space.

That can also mean higher advisory costs at a time when capital is tightly managed.

3. Filing Quality Has Never Mattered More

With increased scrutiny of both quantitative and qualitative variables, the quality of your SEC filings becomes more important than ever.

This includes:

-

S-1 registration statements

-

Financial disclosures

-

XBRL and iXBRL tagging

Errors, inconsistencies, or non-compliant structured data are not merely technical issues. In a setting where Nasdaq considers the broader integrity of your listing package, they can contribute to a pattern of concern.

For further information on structured data requirements, visit here.

4. Less Predictability, More Uncertainty

Meeting quantitative requirements no longer guarantees approval.

For finance teams and boards planning around listing deadlines, this unpredictability makes documentation quality, advisor credibility, and compliance discipline more critical than ever.

Why Filing Quality Is Now a Competitive Advantage

In this new environment, clear, accurate, and well-structured SEC filings are more than compliance documents. They are credibility signals.

Issues such as:

-

iXBRL tagging errors

-

Mismatches between financial statements and structured disclosures

-

Last-minute corrections

Can generate concerns when confidence is essential.

Conversely, a filing that is precise, organized, and technically sound strengthens your overall listing narrative.

What Successful Companies Do Differently

How À La Carte Pricing Helps Companies Navigate This Change

One of the realities of the new listing climate is that costs are increasing when capital is most constrained.

-

A higher float requirement demands more pre-IPO capital.

-

Stricter advisor standards may increase professional fees.

-

Compliance complexity continues to grow.

Flexible, à la carte pricing for SEC filing services provides a practical solution.

Instead of committing to expensive bundled engagements, micro-cap companies can engage experts for specific needs such as:

-

iXBRL tagging for an S-1

-

Financial statement structuring

-

Ongoing 10-K and 10-Q support

This flexibility enables:

-

Cost control without sacrificing quality

-

Access to specialized expertise

-

Scalability as reporting requirements increase

For capital-constrained companies, this approach is more efficient.

Actionable Steps for Your Listing Preparation

If you are advising a micro-cap company planning a Nasdaq listing:

-

Revisit float projections using the $15 million threshold as baseline.

-

Assess advisor relationships for track record strength.

-

Prioritize XBRL and iXBRL compliance early.

-

Engage a reliable SEC filing partner.

-

Create structured review checkpoints within your S-1 timeline.

These steps move preparation from reactive scrambling to disciplined execution.

How DataTracks Helps You Navigate the New Listing Standard

At DataTracks, we understand that SEC reporting for a listing-stage company is a credibility exercise. With over 20 years of regulatory reporting experience and more than 300,000 reports delivered, DataTracks brings institutional knowledge and operational depth that stands up to scrutiny.

Comprehensive SEC Filing Services

DataTracks offers end-to-end SEC filing support including:

-

EDGAR submissions

-

Inline XBRL and iXBRL tagging

-

S-1 preparation support

-

Ongoing compliance for 10-Ks, 10-Qs, and other mandated forms

Learn more here.

DataTracks Rainbow for SEC Reporting

DataTracks Rainbow is a secure, cloud-based iXBRL solution designed specifically for SEC reporting. It automates tagging, enforces taxonomy rules, and performs validations in real time.

Get a demo here.

Flexible, Transparent Pricing

We operate on a transparent, à la carte service model. You engage the expertise you need, at the stage you need it.

Request a tailored quote here.

Final Thought

Nasdaq has raised the bar in two dimensions.

The quantitative threshold has tripled. The process now includes a qualitative layer that evaluates your advisors, comparable trading patterns, and the overall quality signal your filing package delivers.

For micro-cap enterprises and their financial advisors, this is not a reason for concern. It is a call for preparation.

Companies that understand early that filing quality, advisor reputation, and compliance precision are strategic elements, not operational details, will be best positioned to succeed.

The standard is higher. With proper preparation and the right partners, it remains achievable.