In early 2025, a mid-size Southeast Asian technology company finally achieved what it had been working toward for three years: regulatory approval to list on the SGX. The CFO described the moment as “anticlimactic.”

Not because the milestone didn’t matter. But because within six weeks of listing, the company received a regulatory query from ACRA over a tagging error in its first XBRL filing. The error wasn’t financially material. The distraction to the senior leadership team, arriving during a critical post-IPO growth window, was.

This story isn’t exceptional. It is, increasingly, the baseline.

Singapore’s equity markets are in their strongest position since 2019. With over S$2.5 billion raised in 2025 and 20 IPOs forecast for 2026, the momentum is undeniable. Yet, the CFOs most at risk are not those who miss the window – they are the ones who walk through it without understanding that public company compliance is an operating model, not a filing task.

The 2026 Market: High Liquidity, Higher Scrutiny

The market conditions that make 2026 attractive also make the compliance environment more demanding. Three structural changes have redefined the “public” finance function:

Unified Oversight:

Regulatory review is now consolidated under SGX RegCo, concentrating scrutiny and raising the bar for prospectus consistency.

The Dual-Listing Edge:

The SGX–Nasdaq Global Listing Board now allows for a single prospectus for dual listings, increasing international visibility (and the consequences of reporting errors).

Institutional Expectations:

A S$5 billion MAS liquidity injection is attracting institutional investors with active governance expectations. Disclosure quality is now a capital-market signal.

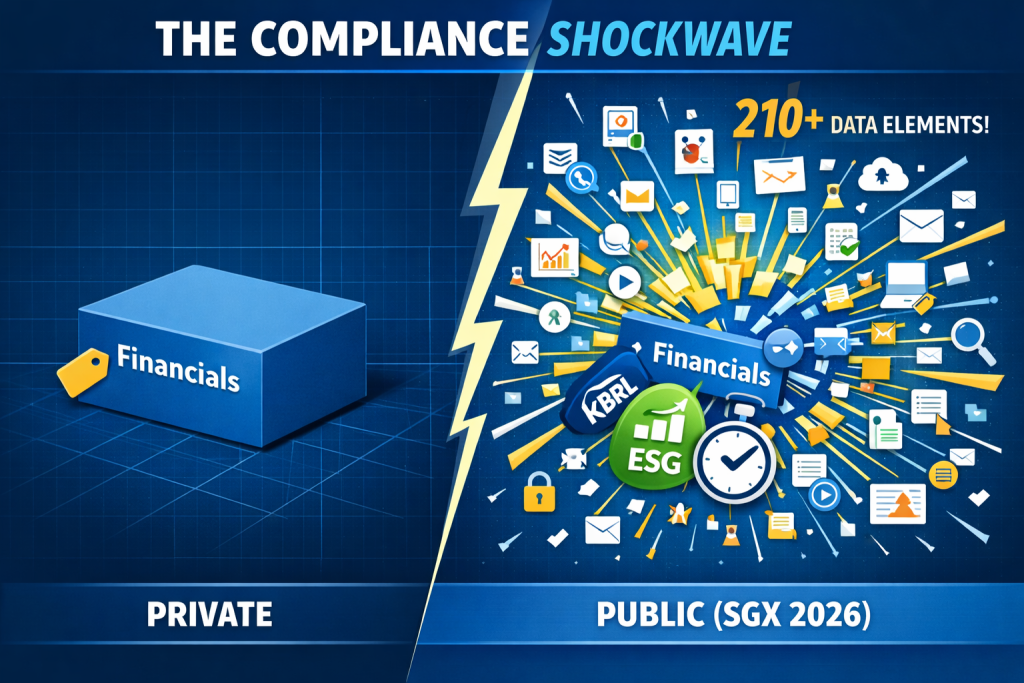

The Mental Shift: Private vs. Public

The reporting model that serves a private company fails almost immediately upon listing. The following table illustrates the structural “shock” many finance teams face in their first year:

| Capability | Private Entity (Standard) | Public Entity (SGX 2026) |

| XBRL Scope | Simplified / Key Data | Full XBRL (210+ elements) |

| ESG Focus | Marketing / Voluntary | Governed (ISSB/IFRS S2) |

| Disclosure | Periodic / Board-led | Immediate / Market-triggered |

| Reviewer | ACRA (Annual) | SGX RegCo (Continuous) |

The Three Pillars of Public Compliance

From day one of listing, the CFO’s desk carries three non-negotiable obligations. Each operates on different timelines, and none tolerate improvisation.

1. Full XBRL Filing (ACRA)

Listed companies must file financial statements in Full XBRL format within five months of year-end. This requires tagging ~210 data elements, including complex element-level tagging for notes such as impairment assessments and related party transactions. Treat this as an extension of “simple” XBRL at your own peril.

2. Mandatory ESG Disclosure (IFRS/ISSB)

From FY2026, SGX-listed companies must comply with IFRS Sustainability Disclosure Standards (ISSB). This is a governed disclosure regime requiring longitudinal data (emissions, energy consumption) gathered throughout the year.

Warning: If your ESG data collection architecture is not already in place for FY2026, your readiness window is narrowing.

3. Continuous Disclosure Obligations

Material announcements under the SGX Listing Manual are event-triggered. The disclosure clock starts when the event becomes known. This requires a “standing infrastructure” to identify, draft, and submit announcements within business hours.

Strategic Roadmap: Five Decisions to Make Before the Bell

These are not checklists; they are foundational process decisions that must be tested during your pre-listing runway.

1. Map Early: Map your financial data to the ACRA Full XBRL taxonomy now. Your prospectus financials will anchor your first filing; if they don’t map cleanly, remediation is public and expensive.

2. Architect, Don’t Assemble: Assign ESG data ownership at the departmental level (Operations, HR, Procurement) for FY2026 collection today.

3. Define the Triggers: Formalize a “materiality decision tree” with legal alignment. Define what triggers disclosure and who owns the announcement clock.

4. Stress-Test the Close: Model your year-end close assuming zero flexibility. Can your team survive the five-month Full XBRL window without burnout or errors?

5. Front-Load Expertise: Engage compliance architecture specialists during IPO prep. Fixing structural weaknesses under the gaze of SGX RegCo costs multiples of building them correctly pre-listing.

Conclusion: Built to Operate

In 2026, the defining differentiator for listed companies will not be valuation multiples alone. It will be disclosure quality and governance resilience. The question for the modern CFO is no longer: “Are we ready to list?” It is: “Are we built to operate in public?”

About DataTracks

DataTracks has supported SGX-listed companies in building structured XBRL and regulatory disclosure infrastructure for over a decade. We prepare approximately 20,000 XBRL statements annually across 26 countries and have delivered 300,000+ reports globally.

Ready to pressure-test your XBRL readiness or ESG data architecture?

Contact our Singapore Team | +65-3158-2850